Can the Eu Continue to Run Current Account Deficits Indefinitely

Current account

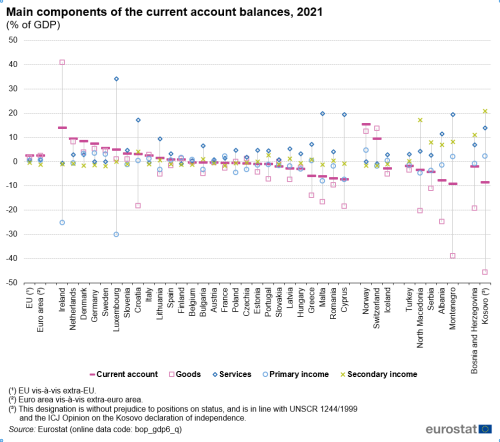

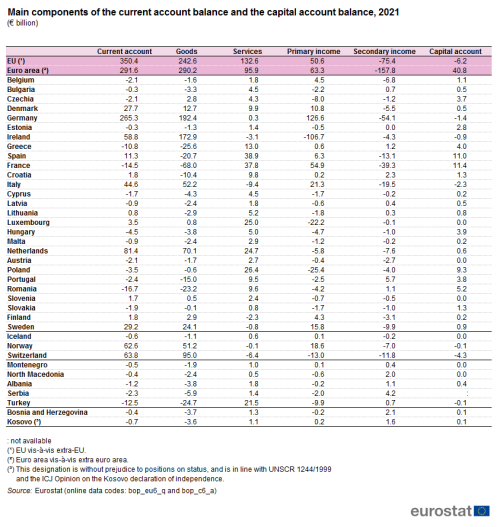

The current account of the EU showed a surplus of €350.4 billion in 2021 (see Figure 1), corresponding to 2.4 % of gross domestic product (GDP). By comparison, in 2020 the current account surplus was €315.9 bn. The surplus in the current account balance for the EU increased significantly since 2010 from 0.6 % of GDP or €64.6 bn to 3.2 % in 2016 or €402.5 bn. Since then, it has been slowly decreasing in absolute values as well as a share of GDP. The current account surplus of the EU for 2021 was mostly based on a significant surplus in the goods account (1.7 % of GDP), while the services account contributed 0.9 % of GDP and the primary income account 0.4 % of GDP to the positive balance while the secondary income account (-0.5 % of GDP) recorded a deficit. The capital account displayed balanced figures (0.0 % of GDP) — see Figure 3.

![]()

Figure 1: Current account transactions, EU, 2010-21

(€ billion)

Source: Eurostat (bop_eu6_q)

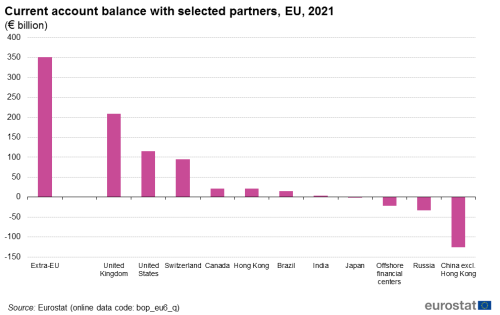

Among the partner countries and regions shown in Figure 2, the EU's current account deficit was by far the largest with China, standing at €125.2 bn in 2021, followed by Russia (€33.2 bn) and offshore financial centres[1] (€21.3 bn). On the other hand, the highest current account surpluses were recorded with the United Kingdom (€209.5 bn), the United States (€114.6 bn) and Switzerland (€95.1 bn). Surpluses were also recorded with Canada, Hong Kong, Brazil and to a minor extent with India.

Figure 2: Current account balance with selected partners, EU, 2021

(€ billion)

Source: Eurostat (bop_eu6_q)

There were 15 EU Member States that reported current account deficits in 2021, and 12 that recorded surpluses (see Figure 3 and Table 1). The largest relative deficits measured as a share of GDP were observed in Cyprus (7.3 %), Romania (7.0 %) and Malta (6.1 %), while Ireland (13.9 %), the Netherlands (9.5 %) and Denmark (8.3 %) reported the largest surpluses relative to GDP in their current accounts. In absolute terms however Germany recorded by far the largest current account surplus (€265.3 bn) and Romania the largest current account deficit (€16.7 bn).

Figure 3: Main components of the current account balances, 2021

(% of GDP)

Source: Eurostat (bop_gdp6_q)

By taking a closer look at the current account components, it becomes apparent that the EU's current account surplus with the rest of the world in 2021 was mostly built upon positive balances in the goods and to a smaller extent in the services and primary income accounts (€242.6 bn, €132.6 bn and €50.6 bn respectively) despite having a negative balance for the secondary income account (€75.4 bn) — see Table 1. The current account surplus for the euro area (€291.6 bn) was generated by a huge surplus in trade in goods (€290.2 bn), considerable positive net exports of services (€95.9 bn), a surplus in primary income (€63.3 bn) and reduced by a significant deficit in secondary income (€157.8 bn). In absolute values Germany (€192.4 bn), Ireland[2] (€172.9 bn) and the Netherlands (€70.1 bn) were the largest net exporters of goods to other countries (intra-EU + extra-EU), while more than half of the EU Member States (17 countries) faced negative balances in their goods accounts in 2021. Among those, France was by far the largest net importer of goods (€68 bn), followed by Greece (€25.6 bn) and Romania (€23.2 bn). The biggest net exporters of services in 2021 were Spain (€38.9 bn), France (€37.8 bn) and Poland (€26.4 bn) while Italy (€9.4 bn), Ireland (€3.1 bn), Finland (€2.3 bn) and Sweden (€0.8 bn) were the only net importers.

Among EFTA countries, Switzerland (€63.8 bn) reported a significant current account surplus in 2021 due to a huge surplus for goods (€95.0 bn) despite considerable negative balances for services (€6.4 bn), primary income (€13.0 bn) and secondary income (€11.8 bn).

Table 1: Main components of the current account balance and the capital account balance, 2021

(€ billion)

Source: Eurostat (bop_eu6_q) and (bop_c6_a)

Altogether 10 Member States recorded surpluses for goods in 2021, while 23 Member States recorded surpluses for services with the rest of the world — see Figure 3. Among those with the largest relative exposure to surpluses in goods were Ireland (41.0 % of GDP), the Netherlands (8.1 % of GDP) and Germany (5.4 % of GDP). The highest relative surpluses in services were measured for Luxembourg (34.1 % of GDP), Malta (19.9 % of GDP) and Cyprus (19.5 % of GDP). The economies with the largest relative net deficit in goods were Cyprus (18.4 % of GDP), Croatia (18.2 % of GDP) and Malta (16.7 % of GDP) and for services Finland (0.9 % of GDP).

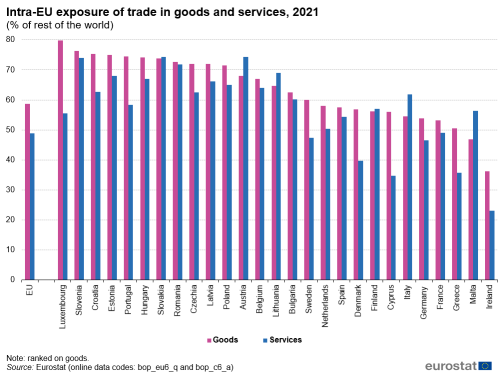

Around 58.7 % of EU Member States' international trade in goods and almost half of their trade in services (48.8 %) were related to trade with other EU countries in 2021 — see Figure 4. Cross-border trade in goods with EU partners was highest in Luxembourg (79.8 %) and 10 other Member States recorded shares of over 70 %. The lowest share was reported by Ireland (36.2 %). Cross-border trade in services with other EU economies was most prominent in Slovakia (74.4 %), Austria (74.3 %) and Slovenia (74.0 %) and lowest in Ireland (23.1 %).

Figure 4: Intra-EU exposure of trade in goods and services, 2021

(% of rest of the world)

Source: Eurostat (bop_eu6_q) and (bop_c6_a)

Capital account

The capital account of the EU displays traditionally a deficit, resulting from considerable net capital transfers to the rest of the world. In 2021, this trend was continued with a capital account deficit of €6.2 bn — see Table 1. Among the Member States, Italy recorded the highest absolute capital account deficit (€2.3 bn, 0.1 % of GDP), whereas significant relative capital account surpluses were reported by Estonia (9.2 %), Hungary (2.5 %), Croatia (2.3 %), Greece (2.2 %) and Romania (2.2 %) mostly due to net receipts from EU institutions.

Financial account

The financial account consists of direct investment (FDI), portfolio investment, other investment, (net) financial derivatives and reserve assets. Financial account transactions are split in assets and liabilities that are recorded as net values (net acquisition of assets, net incurrence of liabilities). Accordingly, the financial account balance is interpreted as net lending to the rest of the world when positive, and net borrowing from the rest of the world when negative.

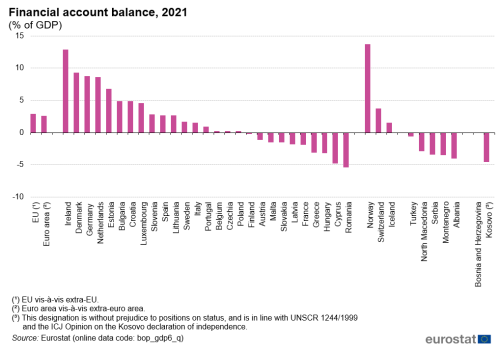

In 2021 the overall net value of the EU financial account was firmly positive (€413.9 bn), as was the net value of the euro area financial account (€316.8 bn). These surpluses related to 2.9 % of GDP (EU) and 2.6 % of GDP (euro area). Apart from the EU and the euro area a total of 17 EU Member States were net lenders to the rest of the world in 2021, showing surpluses in their net financial accounts. The highest value relative to their GDP were reported by Ireland (12.9 %) and Denmark (9.3 %). By contrast, 10 EU Member States were net borrowers, among those Romania (-5.4 % of GDP) exhibited the highest relative deficit in regards to its GDP — see Figure 5.

Figure 5: Financial account balance, 2021

(% of GDP)

Source: Eurostat (bop_gdp6_q)

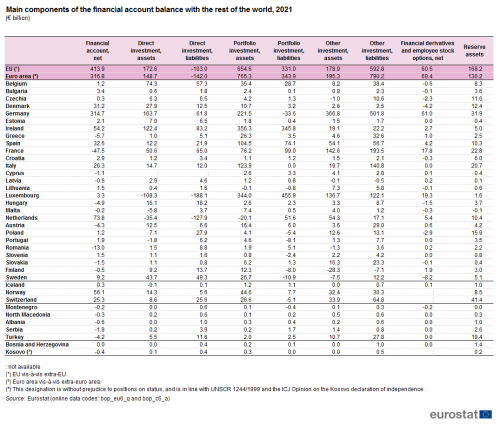

In 2021, the largest net lender in absolute terms in the EU was Germany with €314.7 bn (see Table 2). The German financial surplus was achieved mainly due to net acquisitions of foreign assets in portfolio (€255.1 bn) and direct investment (€101.8 bn) while activities in other investment (-€135 bn) reduced the positive net figure. The major hubs for financial account transactions in the EU in 2021 were Germany, Ireland and Luxembourg.

Table 2: Main components of the financial account balance with the rest of the world, 2021

(€ billion)

Source: Eurostat (bop_eu6_q) and (bop_c6_a)

France was in absolute terms the largest net borrower from the rest of the world in 2021 with a financial account deficit of €47.5 bn (1.9 % of GDP). The negative net financial account of France resulted mainly from net incurrences of liabilities in other investment (€50.9 bn), portfolio investment (€22.8 bn) and direct investment (€14.4 bn) that were much higher than the corresponding net acquisitions in net financial derivatives and employee stock options (€17.8 bn) and reserve assets (€22.8 bn).

For the EU transactions in direct investment (€172.6 bn in acquisitions of net assets and -€103.0 bn in acquisitions of net liabilities) contributed positively (€275.6 bn) to the net financial account value in 2021. Germany recorded the highest transaction values for net acquisitions of assets (€163.7 bn) and Luxembourg for net acquisitions of liabilities (-€188.1 bn) in direct investment. The highest surplus was displayed by Germany (€101.8 bn) and the largest deficit (€20.9 bn) by Poland.

In 2021 the overall net financial account surplus of the EU was mainly supported by transactions in portfolio investment with the rest of the world that displayed €654.6 bn in net acquisitions of assets and only €331.0 bn in net acquisitions of liabilities. Ireland recorded the highest transaction values for net acquisitions of assets (€356.3 bn) and Luxembourg for net acquisitions of liabilities (€455.9 bn). Germany reported the largest surplus (€255.1 bn) and Luxembourg the biggest deficit (€112.0 bn).

For other investment the EU's financial account exhibited in 2021 a significant net deficit of €414 bn. Germany recorded the highest transaction figures for net acquisitions of assets (€366.8 bn) and for net acquisitions of liabilities (€501.8 bn). The Netherlands recorded the highest surplus (€37.2 bn) while Germany (€135.0 bn) and Italy (€121.1 bn) recorded the largest deficits in other investment.

For the EU, financial derivatives and employee stock options component of financial account exhibited a net surplus of €60.5 bn (0.4 % of GDP). Germany (€61.0 bn) displayed the highest positive net figures while Sweden (€8.2 bn) showed the largest net deficit.

Among EFTA countries, Norway recorded by far the highest surplus in the financial account (€56.1 bn). Switzerland (€25.3 bn) and Iceland (€0.3 bn) were also net lenders in 2021. Norway's positive balance in its financial account was determined mainly by considerable surpluses in portfolio investment (€36.9 bn) and in direct investment (€8.7 bn). Switzerland's net lending status was supported mainly by a positive development in reserve assets (€41.4 bn) and net lending in portfolio investment of €31.7 bn while other investment and direct investment activities contributed negatively. Iceland's positive financial account balance with the rest of the world resulted from a surplus in reserve assets.

Data sources

The main methodological reference used for the production of balance of payment statistics is the sixth edition of the Balance of Payments and International Investment Position Manual (BPM6) of the International Monetary Fund (IMF). This set of international standards had been developed, partly in response to important economic developments, including an increased role for globalisation, rising innovation and complexity in financial markets, and a greater emphasis on using the balance sheet as a tool for understanding economic activity (asset–liability principle). The IMF Statistics Department has launched the update of the BPM6 targeting to publish an updated version of the Manual (BPM7) by March 2025. The BPM6 update is being coordinated with the update of the System of National Accounts 2008 (2008 SNA).

The transmission of balance of payments data to Eurostat is covered by Regulation (EC) No 184/2005 on Community statistics concerning balance of payments, international trade in services and foreign direct investment. New data requirements according to the BPM6 are included in Commission Regulation (EU) No 555/2012 of 22 June 2012 and Commission Regulation (EU) No 1013/2016 of 8 June 2016 as an amendment to the above.

In April 2022, the first provisional data for the 4th quarter of 2021 became available, from which the first estimate of the annual results for 2021 have been produced.

Current account

The current account of the balance of payments provides information not only on international trade in goods (traditionally the largest category), but also on international transactions in services, primary and secondary income. For all these transactions, the balance of payments registers the value of credits (exports) and debits (imports). A positive balance — a current account surplus (which applies to the EU since 2009) — shows that an economy is earning more from its international export transactions than spending abroad from import transactions with other economies, and is therefore a net creditor (net exporter) towards the rest of the world.

The current account gauges a country's economic situation in the world, covering all transactions that occur between resident and non-resident entities. More specifically, the four main components of the current account are defined, according to the BPM6, as follows.

- International trade in goods covers general merchandise, net exports of goods under merchanting and non-monetary gold. Exports and imports of goods are recorded on a so-called free-on-board (FOB) valuation — in other words, at market value at the customs frontiers of exporting economies, thus including charges for insurance and transport services up to the frontier of the exporting economy. As a consequence for imports an FOB adjustment is required in order to deduct the value of freight and insurance premiums incurred for the transport up to the border of the importing economy.

- International trade in services consists of the following items: manufacturing services performed on physical inputs owned by others (goods for processing), maintenance and repair services, transport services performed by EU residents for non-EU residents, or vice versa, involving the carriage of passengers, the movement of goods, and auxiliary services, such as cargo handling charges, packing and repackaging, towing not included in freight services, pilotage and navigational aid for carriers, air traffic control, salvage operations, agents' fees, and so on; travel, which includes primarily the goods and services EU travelers acquire from non-EU residents, or vice versa; and other services, which include construction services, insurance and pension services, financial services, charges for the use of intellectual property not included elsewhere, telecommunications, computer and information services, other business services (which comprise research and development services, professional and management consulting services, technical and other trade-related services, personal, cultural and recreational services, and government services not included elsewhere).

- Primary income covers basically three types of transactions: compensation of employees paid to non-resident workers or received from non-resident employers, investment income from direct, portfolio, other investment and reserve assets, and other primary income (taxes on production and on imports, subsidies and rent). All investment income components cover income on equity and investment fund shares (divided between distributed and accrued income) and interest from investment in debt securities, deposits or loans, and investment withdrawals from income of quasi-corporations.

- Secondary income includes general government current transfers, for example payments of current taxes on income and wealth, social contributions and benefits, transfers related to international cooperation, and current transfers related to financial and non-financial corporations, households, or non-profit organisations.

Capital account

The capital account of the balance of payments provides information on the acquisition of non-financial assets by residents in the rest of the world, or by non-residents in the compiling economy, for example investment in real estate. It also includes capital transfers by general government and financial, non-financial corporations, households or non-profit organisations (also specifically covering debt forgiveness).

Financial account

The financial account of the balance of payments covers all transactions associated with changes of ownership in financial assets and liabilities of an economy with the rest of the world. The financial account is broken down, according to the BPM6, into five main components: direct investment, portfolio investment, financial derivatives, other investment, and reserve assets. All components are now recorded according to the asset–liability principle, which supports the full implementation of the balance sheet approach in the financial account. In this regard, net values are recorded and have to be interpreted by keeping the underlying gross transactions in mind — net acquisition of assets is based on the acquisition of new assets minus the sale of assets during the observed period, while net incurrence of liabilities consists of the issue of new liabilities minus redemptions of outstanding liabilities. The resulting balance of net assets minus net liabilities is interpreted as net lending to the rest of the world when positive, or net borrowing when negative.

Direct investment implies that a resident direct investor makes an investment that gives control or a significant degree of influence on the management of an enterprise in another economy. Within this classification FDI in equity/investment fund shares (plus reinvestment of earnings where applicable) and in debt securities are distinguished. A breakdown is required for transactions by direct investor in direct investment enterprises, reverse investments and international transactions between fellow enterprises with the ultimate controlling parent being either resident or non-resident. More aspects are covered in dedicated articles on foreign direct investment (in chapter 4).

Portfolio investment records the transactions in negotiable financial securities with the exception of the transactions which fall within the definition of direct investment or reserve assets. Two main components are identified: equity securities and debt securities (bonds and notes or money market instruments).

Financial derivatives (other than reserves) are financial instruments that are linked to another specific financial instrument, indicator or commodity, and through which specific financial risks can be traded in financial markets in their own right. Transactions in financial derivatives are treated as separate transactions, rather than integral parts of the value of underlying transactions to which they may be linked. They are disseminated as net value of assets and liabilities only.

Other investment is a residual category, which is not recorded under the other headings of the financial account (direct investment, portfolio investment, financial derivatives or reserve assets) and in principal covers four types of instruments — currency and deposits (in general, the most significant item), trade credits/advances, loans, and other assets and liabilities.

Reserve assets are foreign financial assets available to and controlled by monetary authorities; they are used for financing and regulating payments imbalances or for other purposes.

Context

The EU is a major player in the global economy for international trade in goods and services, as well as foreign investment. Balance of payments statistics give a complete picture of all external transactions for the EU and its individual Member States. Indeed, these statistics may be used as a tool to study the international exposure of different parts of the EU's economy, indicating its comparative advantages and disadvantages with the rest of the world, and to calibrate the implied macroeconomic risks for the economy. The financial and economic crisis 2007-2008 underlined the importance of developing such economic statistics insofar as improvements in the availability of data on the real and financial economies of the world could have helped policymakers and analysts when the crisis unfolded; for example, if internationally comparable information about financial transactions and exposure in specific assets and liabilities had been available earlier.

The European Commission launched new policy proposals in this domain aiming to stimulate the economic recovery (such as the European Fund for Strategic Investments), and to launch regular initiatives to calibrate macroeconomic risks in the EU Member States (such as the Macroeconomic imbalance procedure). Further details on the European Commission's initiatives are available from the website of the European Commission's Directorate-General for Economic and Financial Affairs, where more detailed information may be found on a range of recent priorities, for example Growth and Investment and the The European semester.

whiteherhatiought.blogspot.com

Source: https://ec.europa.eu/eurostat/statistics-explained/index.php/Balance_of_payment_statistics

Belum ada Komentar untuk "Can the Eu Continue to Run Current Account Deficits Indefinitely"

Posting Komentar